Introduction to trading mechanisms in the European equities market: Closing Auctions

0

Published:

December 19, 2023

Most recent

Max Wildenberg, Senior Associate, Aquis Markets

As you will remember from our first blog on the topic of ‘Trading Mechanisms – Lit Continuous Trading’, and by way of a recap; approximately €40bn of equities stocks and shares are traded on exchanges across Europe on a daily basis. Generally, this trading flow interacting on exchange can be classified as either Agency or Proprietary flow (sent by firms with or without underlying clients respectively).

To protect the end investors’ best interests, firms trading on behalf of clients are mandated to adhere to regulatory ‘Best Execution’ requirements when deciding in what manner they trade.

To do so, firms must give due consideration to the following factors (in no particular order):

• Price at which the trade occurs

• Cost of execution

• Speed of execution

• Likelihood of execution

• Cost of execution

• Speed of execution

• Likelihood of execution

To assist firms in achieving best execution for the end investor, most European trading venues offer their members (trading firms) a variety of different mechanisms by which their orders to buy or sell a stock can be matched with opposing liquidity (orders). Each trading mechanism has its own optimal use case.

This blog introduces and explains the mechanics of Europe’s second most popular trading mechanism: closing auctions. In addition, we once again explore how trading firms leverage the unique features of this mechanism to meet their best execution requirements.

Closing Auctions

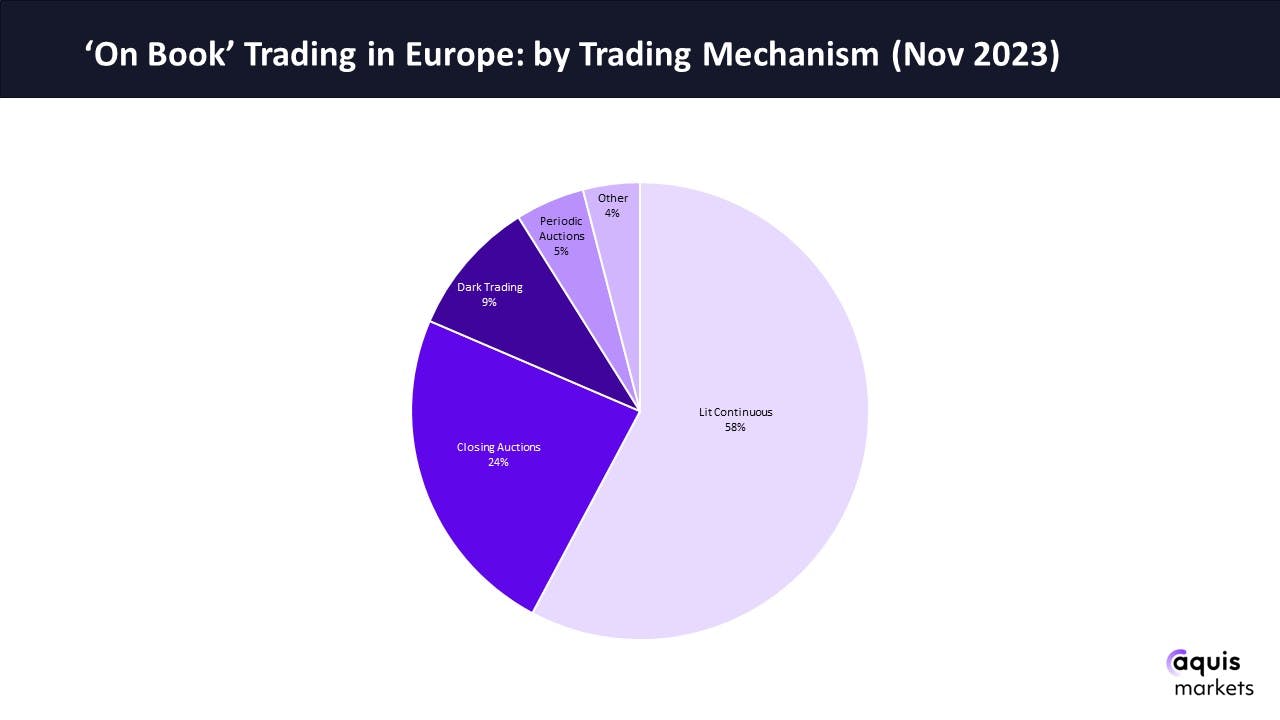

On average, approximately a quarter of all value traded on European exchanges executes at the close - a figure that continues to rise. Certain days, such as index rebalances, see even more volume during the close than throughout the entire continuous trading day.

It is therefore worth understanding what closing auctions are and how they work.

Currently, every equities exchange in Europe has fixed trading hours. As an example, Aquis Markets, where approximately 5% of all European equities are traded, opens for trading at 08:00GMT and closes at 16:35GMT. When the market is closed, trading firms cannot enter any orders to buy or sell and no trading takes place.

The closing price is the price displayed for a given stock while the market is closed. This is the final price at which a given security traded during the trading day. The closing price is a key reference point used by investors to analyse a stock’s performance, used by many across the industry as an important benchmark.

The closing auction is the daily process by which the closing price for a given security is determined. At the end of the trading day the market of listing (the ‘primary’ exchange, where the security is listed) will halt lit continuous trading and will start their closing auction process. Generally, these auctions last for 5 minutes, with exceptions for certain European markets. No trading takes place during this period; instead demand to buy or sell at various price points is collected.

The objective is to identify the most popular and reliable price for a security. An algorithm takes all orders input into the auction into account and calculates the price point at which the highest number of shares would be traded and then execute trades at this uncrossing price at the end of the auction.

Starting from the beginning of the auction and moving chronologically we will explain, in general terms, how most European exchanges’ closing auctions work:

Auction start

A closing auction for each security (stock) on the market of listing begins at the end of lit continuous trading each day. To use the UK market as an example, this occurs at 16:30 GMT.

A closing auction for each security (stock) on the market of listing begins at the end of lit continuous trading each day. To use the UK market as an example, this occurs at 16:30 GMT.

Trading firms can interact with the closing auction by sending orders to the exchange during the auction call phase, the 5 (or 10 for some European markets) minute period between the end of lit continuous trading and the uncrossing of the closing auction at the closing price. In the UK, the auction call phase is between 16:30 and 16:35.

Order entry

Firms have a choice of sending either ‘Market’ or ‘Limit’ orders into the auction call.

Firms have a choice of sending either ‘Market’ or ‘Limit’ orders into the auction call.

-

Market orders are instructions to buy or sell at the market’s current best available price. Trading firms will specify details of the side (buy or sell) and size (number of shares) of their order.

-

Limit orders allow trading firms to add a ‘limit’, in addition to the details of side and size of their order. For bids this limit represents the highest price a firm is willing to buy for, and for an offer it represents the lowest price they are willing to sell for.

Trading firms might choose to use limit orders to control the price at which they can execute, or to influence the final uncrossing price of the auction. Market orders will simply execute at the uncrossing price if the size requirements are met by opposing liquidity.

In the closing auction, market orders have priority for matching ahead of limit orders.

Remember, the closing auction for each security will only uncross at one price. Whether a trading firm submitted a market or limit order, the price of execution will be no different.

Price formation

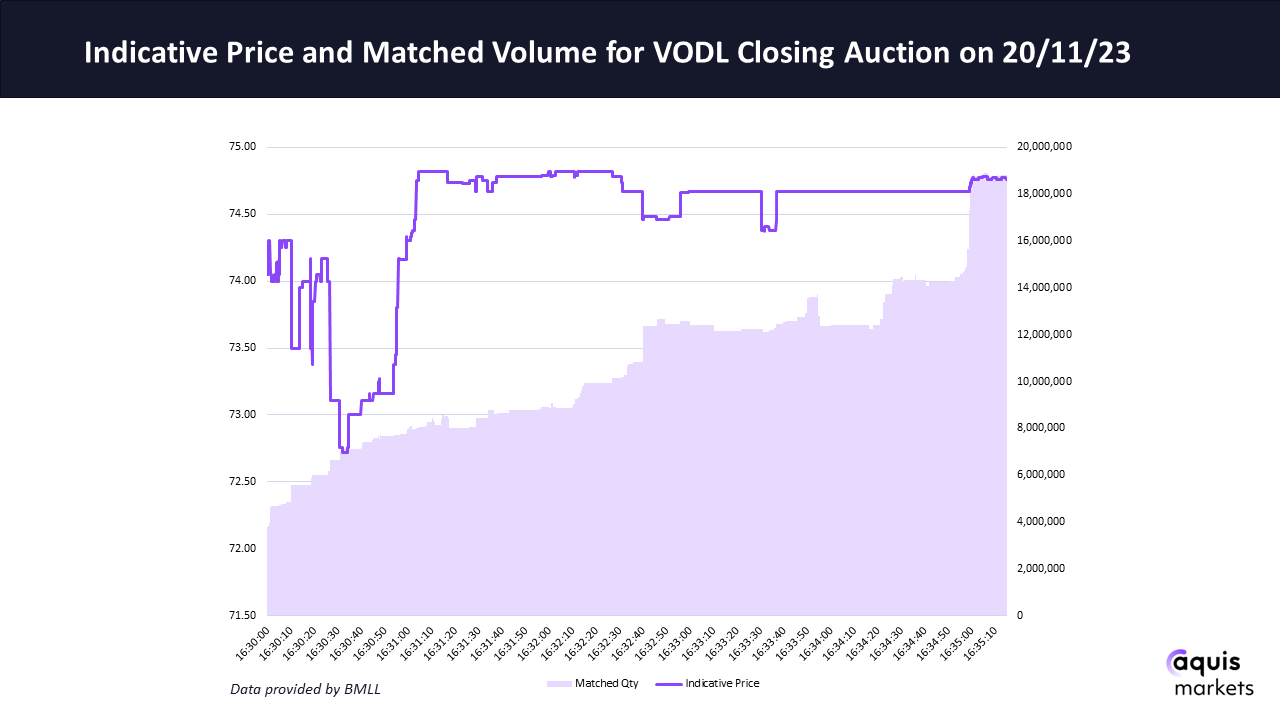

Every order that enters the book will be considered by the auction algorithm. Throughout the auction call period as orders are added, cancelled or modified, the algorithm will recalculate and update the indicative uncrossing price. For any instant, this is the price at which the auction would uncross if there were no more changes to the book.

Every order that enters the book will be considered by the auction algorithm. Throughout the auction call period as orders are added, cancelled or modified, the algorithm will recalculate and update the indicative uncrossing price. For any instant, this is the price at which the auction would uncross if there were no more changes to the book.

This indicative uncrossing price and the number of shares that would trade in the auction are visible to trading members through public market data messages published by the exchange. See below an example of the changes in indicative price and volume a trading firm would observe over the course of a closing auction call phase for a given security.

Uncrossing

The auction will uncross at the end of the auction call phase. Exchanges will randomise exactly when this happens, to minimise the possibility for trading firms to ‘game’ the auction by removing or adding orders just before the end of the auction.

The auction will uncross at the end of the auction call phase. Exchanges will randomise exactly when this happens, to minimise the possibility for trading firms to ‘game’ the auction by removing or adding orders just before the end of the auction.

The randomised period over which the auction uncrosses varies between exchanges. Generally, the auction will uncross within 0-30 seconds after the end of the call period, with certain European exchanges going longer. Using the UK example, this occurs around 16:35:30.

At uncrossing, orders will be executed at the same closing price with the following priority for allocation:

1. Market orders match against opposing market orders.

If there is an imbalance of market orders, for example more market orders to buy than to sell the stock, then…

2. Market orders match against opposing limit orders with price/time priority.

Meaning, in our example the excess market orders to buy will be prioritised to trade against the sell limit orders with the lowest limit price. For orders with the same limit price, the first order to have been sent to the book will be prioritised. Once all market orders have been allocated, then…

3. Limit orders match against limit orders with price/time priority.

If there are only market orders present on the book, the auction will not uncross as a price cannot be formed. In this rare case most European exchanges will use the last traded price during the continuous trading session as the official closing price.

Extensions

A number of European exchanges employ an ‘extension’ mechanism to manage large swings in price during the auction call period.

A number of European exchanges employ an ‘extension’ mechanism to manage large swings in price during the auction call period.

An extension will be triggered if the auction fails to generate a price within a predetermined percentage above or below the last traded price in lit continuous trading.

Each exchange has a slightly different auction extension process. Generally, the auction call period will be extended past the usual uncrossing period allowing orders to be added, removed, and amended for a longer period of time.

These extensions are designed to focus attention onto large price changes and give traders the opportunity to reassess their orders. The ultimate goal is to ensure the final closing price is fair and reliable.

Importance of the closing auction

The closing auction is the most keenly monitored period of the entire trading day. The auction brings together vast numbers of orders from multiple trading firms. The process is vitally important to the entire equities ecosystem with the resulting closing price widely used in financial reporting, fund benchmarking, and in the calculation of indices.

The auction mechanism is a democratic solution to determine the closing price of a security. All trading participants have the opportunity to submit their orders during the call period and every order submitted is considered by the auction algorithm. In addition, all orders that trade in the auction execute at the same time, which effectively levels the playing field, negating the advantage that more technically advanced firms with low latency technology hold in lit continuous trading.

The closing auction also contributes to reducing end of day volatility. By allowing market participants to submit orders during a single, fixed window, it helps prevent last-minute rushes and erratic price movements that can occur in the absence of a structured closing mechanism.

The close is unique in that all orders that trade execute at the same price and time, for this reason best execution considerations differ from intra day trading. However, trading firms do still have decisions to make. For example, the choice as to which order type they use. As mentioned previously, firms looking to maximise likelihood of execution will send market orders into the auction, whereas those looking to control the price at which they execute will use limit orders. In addition, firms looking to minimise their cost of execution also have the choice of sending their orders to one of a number of alternative closing auction mechanisms run by independent exchanges. These enable firms to trade after the end of lit continuous trading at the official closing price for a fraction of the cost charged by the incumbent primary exchanges. Aquis’ own Market at Close product has been the most successful of these, representing approximately 5% of the value traded at the close (at the time of writing).

This blog is the second in a series of explainers on the largest trading mechanisms used across the European equities market which we hope will help readers to build a picture of the entire trading landscape as it exists today.

More information on Aquis Markets order types, including lit, dark, periodic auction and closing auction mechanisms, is available on the ‘products’ section of our website. For any questions for the author, please contact Max on sales@aquis.eu.