Introduction to trading mechanisms in the European equities market: Lit Continuous Trading

0

Published:

October 17, 2023

Most recent

Max Wildenberg, Senior Associate, Aquis Markets

The world of equities trading can often feel like a mysterious “black box” to those who don’t work in financial services – or indeed do, but don’t directly engage with the market. The equities landscape - which Aquis is a key part of - represents a major component of capital markets and the wider global economy.

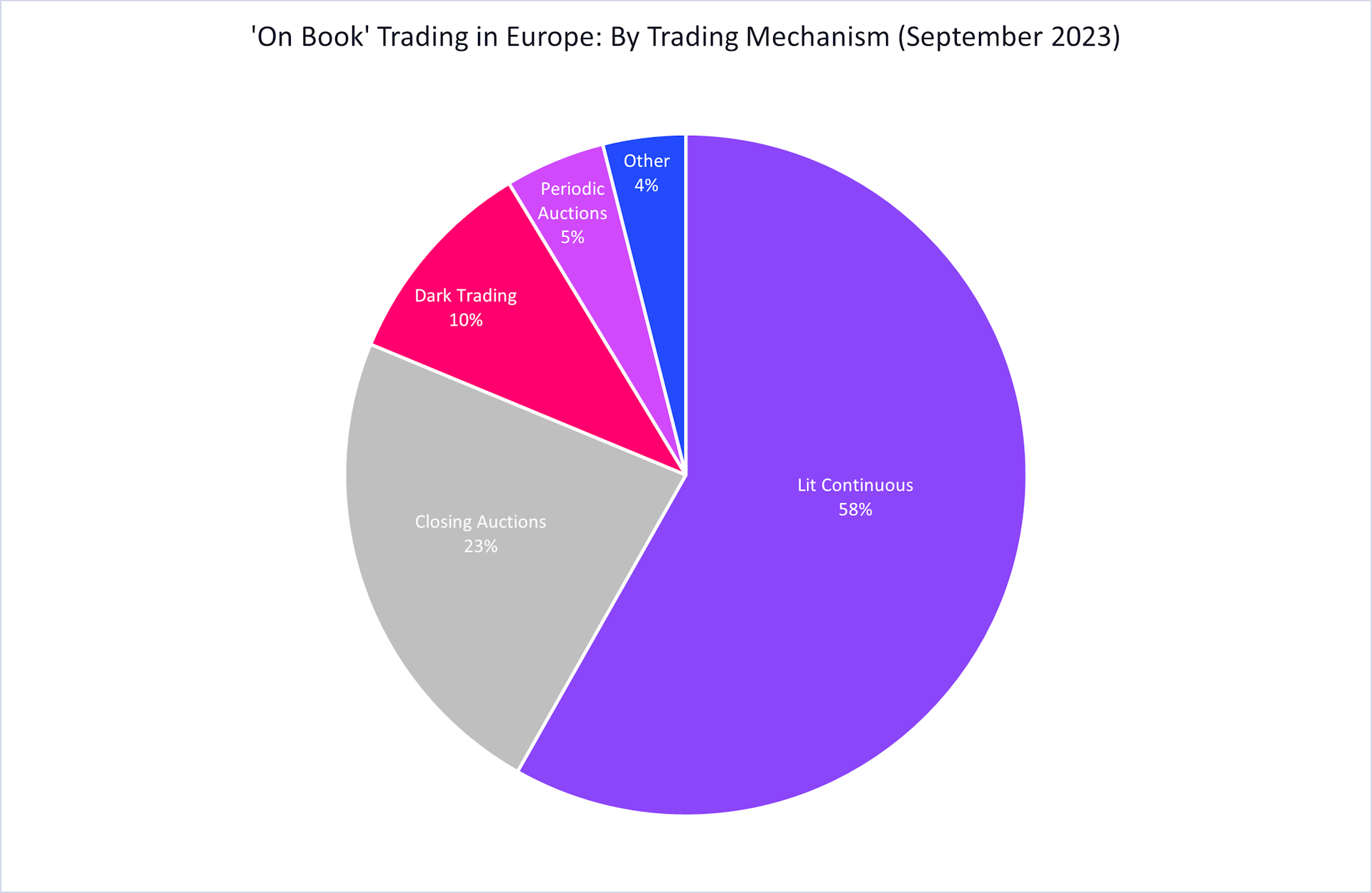

Approximately €40bn of equities, also known as stocks and shares, are traded on exchanges across Europe on a daily basis. Trading firms have the choice of multiple exchanges where they can send orders to buy or sell European securities. Aquis Markets is one such venue, where around €2bn of this trading activity takes place each day.

Generally, all €40bn of this trading flow interacting on exchange can be classified into one of two categories.

- Agency flow – sent by firms trading on behalf of their underlying clients. These traders/brokers will buy or sell stock depending on the requirements of the likes of pension funds, wealth funds and retail investors (their clients). Agency firms make money through commission paid to them for executing trades.

- Proprietary flow – sent by firms trading on their own behalf rather than for underlying clients. These traders aim to profit from the changes in stock prices and spreads over time. They do not receive commission for their trades.

The European equities market is incredibly dynamic. Throughout the trading day, a number of factors can influence the price of a security and these trading firms are faced with multiple choices as to where, when and how to buy or sell a stock. In order to protect the end investor’s best interests, firms trading on behalf of clients are mandated by regulation to adhere to a set of ‘best execution’ requirements when deciding in what manner they trade.

Best execution rules as specified by the Markets in Financial Instruments Directive 2014 (or MiFID 2) require firms to “use reasonable diligence to ascertain the best market for the subject security, and buy or sell in such market so that the resultant price to the customer is as favourable as possible under prevailing market conditions” (The FCA mirror these requirements in COBS 11.2A ‘Best Execution – MiFID provisions’)

In order to do so, firms must give due consideration to (in no particular order);

• Price at which the trade occurs

• Cost of execution

• Speed of execution

• Likelihood of execution

• Price at which the trade occurs

• Cost of execution

• Speed of execution

• Likelihood of execution

To assist firms in achieving best execution for the end investor, most European trading venues offer their members (trading firms) a variety of different mechanisms by which their orders to buy or sell a stock are matched with opposing liquidity (orders). Each trading mechanism has its own merits. This blog provides a brief introduction to the most popular mechanisms used by European firms.

Lit Continuous Trading – the CLOB

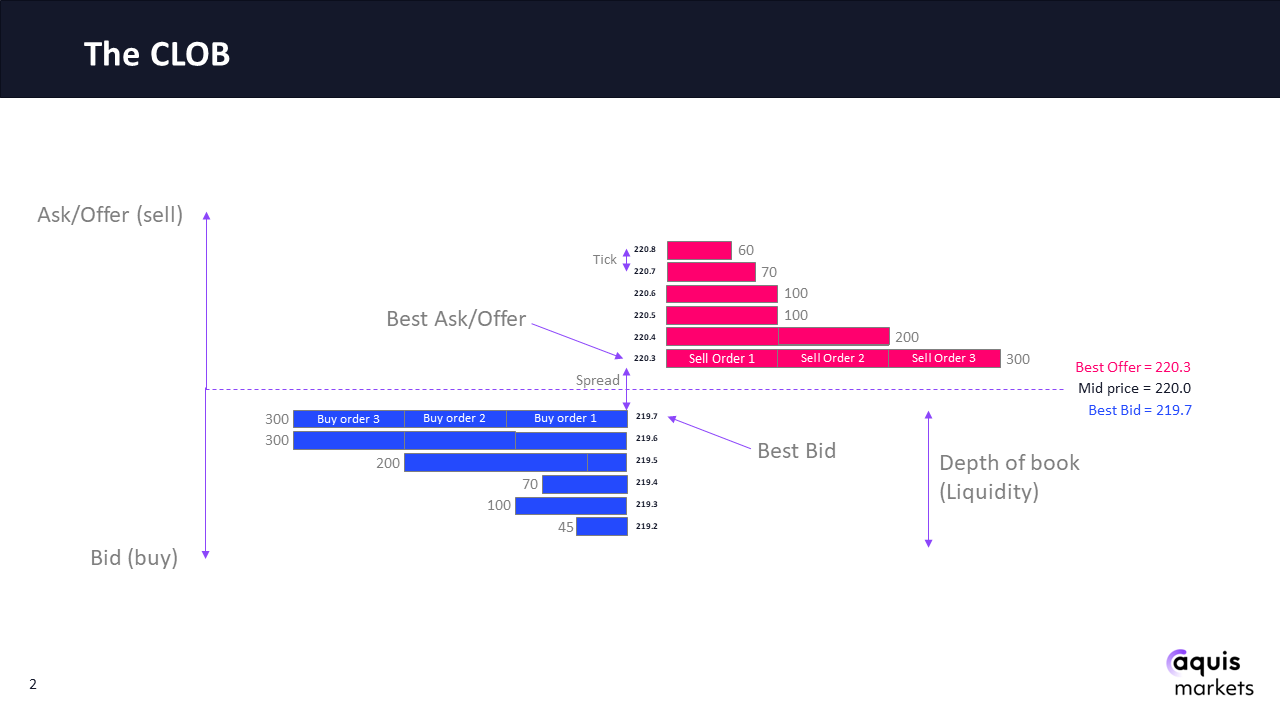

Lit Continuous Trading is the most popular trading mechanism in Europe by value traded. Here, trading firms submit their bids (buy) and offers (sell) to a Central Limit Order Book (CLOB). The CLOB is a pre-trade transparent process by which trading firms’ bids and offers are matched with price/time/size priority. It has formed the basis of trading since the electronification of stock exchanges.

The diagram above is an example of a CLOB for one particular security on a given exchange. There are a number of features that are worth explaining. Starting with the fundamentals and building upon these:

- Firstly, there are two ‘sides’ of the book. The ‘bid’ – comprised of orders submitted by firms wanting to buy the stock, and the ‘offer’ - comprised of orders submitted by firms wanting to sell the stock.

- Trading firms can submit orders at various different ‘price levels’. The difference between each price level is called the ‘tick’. The example above shows a tick size of 0.1.

- Members can specify the price at which they are willing to execute by adding a ‘limit’ to their order. For bids this limit represents the highest price a firm is willing to buy for, and for an offer the lowest price they are willing to sell for.

- Multiple orders from different firms may sit at the same price level. The order that arrived first will sit at the ‘front of the queue’ and has priority for execution (trading). In the diagram above the first orders submitted are displayed closer to the centre of the X axis.

- The cumulative number of shares represented at each price level is referred to as the ‘size’ or ‘quantity’ available. The number of price levels with orders is called the ‘depth of book’.

- The highest price at which anyone is willing to buy is the ‘best bid’. The lowest price at which anyone is willing to sell is the ‘best offer’. In this particular example the best bid is 219.7 and the best offer 220.3.

- A buy and a sell order at the same price level will result in a trade. For this reason, there will always be a difference between the best bid and the best offer, which is referred to as the ‘spread’. In this example the spread is 0.6, between 219.7 bid and 220.3 offer.

- The ‘midpoint price’ is the mid point between the best bid and the best offer. In this example the midpoint price is 220.0.

There are two distinct ways that trading firms are able to interact with the order book: aggressively or passively.

An aggressive buy or sell order would remove existing liquidity (orders) from the book. Using our example, an aggressive order to buy 100 shares at market (the best price available to sell) would see 100 shares removed from the offer side of the book. This scenario is sometimes called ‘crossing the spread’ as the buy order is crossing over to interact with the sell side of the book.

The execution priority of the order book determines which of the resting sell orders this aggressive order will trade with. The CLOB has a price/time/size priority so this incoming order will first interact with the lowest price level (220.3) and the first order submitted at that price level (Sell Order 1).

Above shows an aggressive trade: the incoming buy order trades with Sell Order 1 and therefore removes this liquidity from the book.

An aggressive order can interact with multiple orders across multiple price levels, depending on the size and price limit specified by the trading firm.

A passive buy or sell order would add liquidity (orders) to the book. Using our example, a firm could choose to submit a buy order for 100 shares with a limit price of 219.5. This order would not immediately interact with the offer side of the book, it would not cross the spread, and would therefore rest on the bid side.

This passive order is the most recent order submitted at the price level and for this reason it will join the back of the queue of priority. If an incoming aggressive order to sell were submitted to the book, our new passive order would only execute (trade) once the existing resting buy orders at the price levels 219.7, 219.6 and 219.5 have been removed or cancelled (due to price/time/size prioritisation).

A passive order does not have to be filled in full for a trade to happen. When interacting with an opposing order of smaller size a partial fill occurs, and the remaining portion of the passive order would rest on the book.

The CLOB affords a number of advantages which will assist trading firms in achieving best execution.

- Pre-trade transparency offers a clear picture of fair price. The fact that the order book is completely transparent and trading firms can see the orders at every price level enables traders to build a clear understanding of demand to buy or sell a given stock. The number of orders on each side of the book will also serve as indicators for likely directional movements in price. For example, an imbalance in orders to buy a stock (more orders to buy than sell) would suggest there is more demand than supply for a stock, which will in turn lead to a price increase.

- High likelihood of execution. Trading firms targeting resting liquidity on the CLOB and looking to trade aggressively know their order will execute as long as it reaches the exchange before the resting liquidity is taken by another incoming order.

- High speed trading. Faster trading and more certainty, relative to other mechanisms that will be covered in the next posts in this series.

In addition to these best execution benefits, the Central Limit Order Book is a key foundation of modern equities markets. If the role of a market is to determine an accurate price for a security in any given instant through the balance of demand and supply, a transparent and centralized system by which buyers and sellers can meet is of fundamental importance. It is for this reason that CLOB prices are used as reference prices for many other trading mechanisms.

This being said, there are some scenarios where trading firms could be better served by other trading mechanisms. Dependant on the intentions/strategy of the trading firm and how they prioritise the best execution factors, the CLOB might not always be considered optimal for certain orders. A couple of examples below:

- Information leakage. The fact that the order book is completely transparent and trading firms can see the orders at every price level means that firms posting liquidity on either side of the book will be giving information away about their intentions to buy or sell a given security. For example, if a firm were to post a large buy order onto the order book, all firms consuming market data from the exchange will know that there is a buyer in the market. It is likely that firms will adjust their offers accordingly and the price of the security will increase as a result. Other trading mechanisms such as dark pools and periodic auctions have lower levels of pre-trade transparency and would therefore be more suitable to firms wishing to minimise information leakage when sending larger orders.

- Impact of latency. CLOBs operate on price/time/size priority. For this reason, the faster a firm is able to send orders from their system to the exchange’s order book, the higher likelihood of execution. This generally means that smaller firms, or firms with less sophisticated technology, will be at a disadvantage to their bigger, more advanced peers. Auction mechanisms are a useful tool these firms can utilise to negate the impact of latency on their trading.

This blog is the first in a series of explainers on the largest trading mechanisms used across the European equities market which we hope will help readers to build a picture of the entire trading landscape as it exists today.

More information on Aquis Markets order types, including lit, dark, periodic auction and closing auction mechanisms, is available on the ‘products’ section of our website. For any questions for the author, please contact Max on sales@aquis.eu.